Cryptocurrency wallets are the gateway for users to store, send, and receive virtual assets. However, running a wallet service legally requires strict compliance with global financial laws. In fact, international standards (notably FATF Recommendation 15) now treat crypto custody and exchange services as Virtual Asset Service Providers (VASPs) subject to anti-money laundering (AML/CFT) regulations. This guide explains what VASP compliance entails and outlines the steps fintech founders and startup owners must follow to register a crypto wallet service legally. You will learn the key requirements, procedural steps, and best practices needed to launch and operate a crypto wallet business in full compliance with AML/KYC rules.

VASPs including crypto wallet providers, must obtain formal authorization in most jurisdictions. For example, the FATF explicitly requires VASPs to be “licensed or registered” for AML/CFT purposes. Similarly, the UK Financial Conduct Authority (FCA) states:

“You must register with us if you want to provide crypto services that come within scope of the money laundering regulations.”f

Failure to register can lead to serious legal penalties. In Ireland, for instance, it is a criminal offense to run a wallet or other VASP activity without registering with the Central Bank. By following the guidance below, readers will understand why legal registration matters, and exactly how to register a crypto wallet service under the relevant VASP licensing regimes.

Understanding Crypto Wallet Services and VASP Compliance

A crypto wallet service generally refers to any business that holds, transfers, or exchanges cryptocurrencies on behalf of customers. This includes custodial wallets (where the service holds private keys or funds for users), payment platforms, and exchanges. Under FATF and many national rules, such activities qualify the business as a Virtual Asset Service Provider (VASP). The FATF guidance notes that VASPs must implement robust AML/CFT controls and be subject to “effective systems for monitoring or supervision”.

In practical terms, a wallet provider typically needs to register as a VASP in its operating jurisdictions. For example, the Irish Criminal Justice Act explicitly lists “custodian wallet provider” among activities that trigger VASP registration. Similarly, U.S. regulators treat most crypto wallet businesses as Money Services Businesses (MSBs) requiring FinCEN registration and AML programs. (For instance, any U.S. wallet that transmits or converts virtual currency must register as an MSB and maintain an AML program under the Bank Secrecy Act.) As FATF explains, a licensed or registered VASP must follow the full set of financial industry obligations, just like banks or broker-dealers.

“The amended FATF Recommendation 15 requires that VASPs be regulated for anti-money laundering… purposes, licensed or registered…”

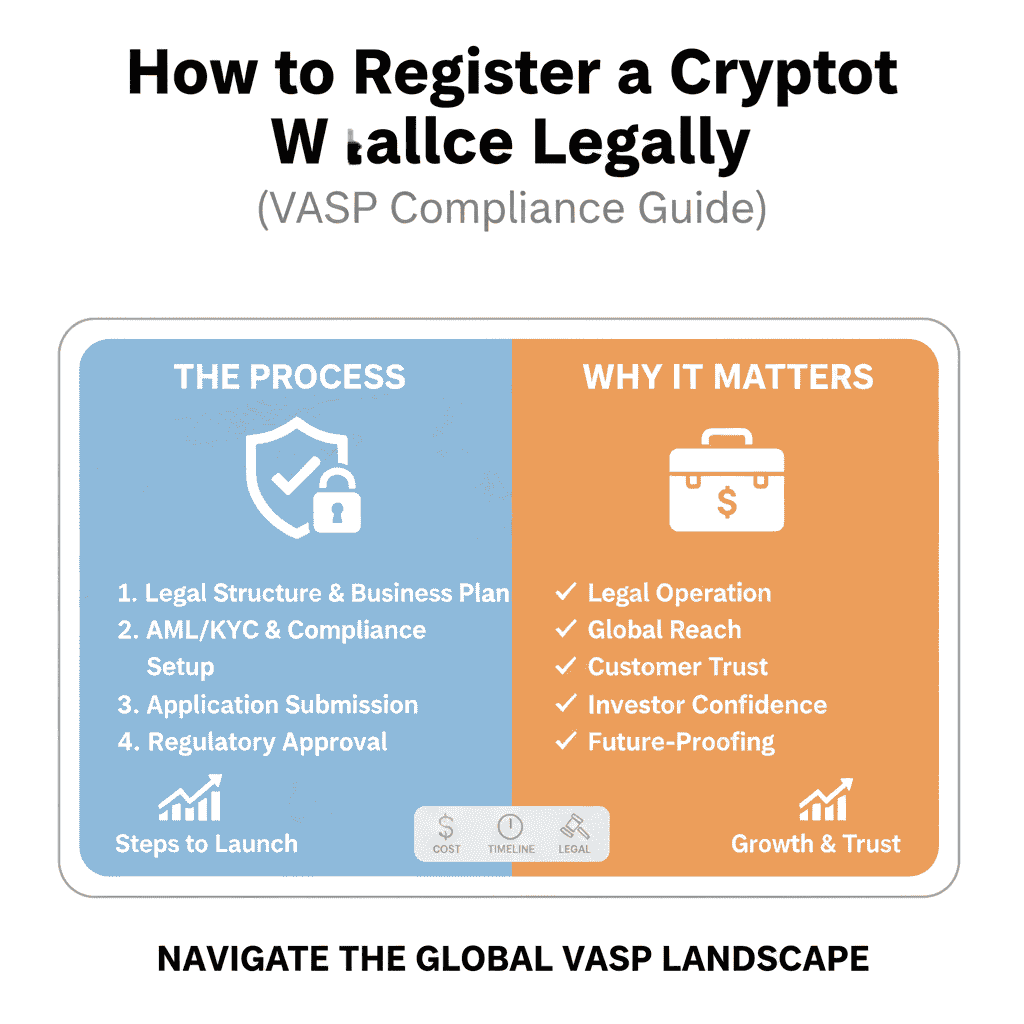

Being recognized as a VASP means the wallet business is legally obligated to identify and verify its users, monitor transactions, report suspicious activity, and cooperate with regulators. In return, compliance enables the company to open corporate banking, partner with payment processors, and build trust with customers and investors. The remainder of this guide will walk through the registration process and compliance safeguards in detail.

Why Legal Registration is Critical

Operating without the required VASP license or registration poses high risks. Regulators worldwide are actively cracking down on unregistered crypto services. In many countries, the law is unambiguous: you cannot offer custody or transfer of virtual assets without permission. For example, the Irish Central Bank’s AML guidance flatly states:

“It is an offence under section 106E (2) of the CJA 2010 to 2021 for a person to carry on the activity of a VASP without registering with the Central Bank.”

Similarly, the FCA warns firms that providing crypto services within scope of AML regulations requires them to register with the agency. Failing to do so can result in civil fines, enforcement actions, or even criminal charges, not to mention reputational damage. In essence, registration legitimizes your business and protects it from legal jeopardy.

Beyond avoiding penalties, formal registration brings concrete benefits: compliant VASPs can access banking services and global payment networks. Licensed status often signals trust to users, investors, and partners. It also signals to regulators and banks that the business adheres to AML and cybersecurity standards, reducing friction in growth and fundraising. In short, legal registration is not just a checkbox—it is a business enabler. It demonstrates to stakeholders and customers that the company operates responsibly under the law.

Steps to Legally Register Your Crypto Wallet Service

Registering a crypto wallet service (i.e. obtaining the required VASP license/registration) involves multiple coordinated steps. While specific processes vary by country, the general procedure includes forming a legal entity, building compliance frameworks, and submitting an application to the appropriate regulator. The key steps are summarized below:

- Form a Legal Entity: Incorporate your company in the jurisdiction where you seek licensure. This usually involves choosing a corporate structure (e.g. LLC or corporation), appointing directors, and registering with local authorities. Prepare corporate documentation such as articles of incorporation, director/shareholder IDs, and proof of address. Many regulators (e.g. Lithuania, Estonia) require this company to be local or to have a local authorized representative.

- Prepare Compliance Program: Develop a robust AML/CFT framework before applying. This includes drafting KYC (Know Your Customer) procedures, risk assessment policies, transaction monitoring plans, and appointing qualified compliance personnel (e.g. an MLRO – Money Laundering Reporting Officer). Ensure you have policies for customer identification, recordkeeping, suspicious activity reporting, and sanctions screening. As FATF guidance emphasizes, your preventive measures (KYC, record-keeping, and STR reporting) will be reviewed during registration.

- Gather Required Documentation: Compile all documents for the application. Typical requirements include a detailed business plan, financial forecasts, technology and security descriptions, AML/CFT policy manuals, shareholder background checks, and sometimes a legal opinion confirming your activities fall under VASP definitions. Cross-border or multi-language issues may arise if your team is international – plan to translate or notarize docs as needed.

- Submit the VASP Application: File the registration or license application with the designated regulator. Many countries use an online portal (for example, Ireland’s Central Bank ONR system). Complete every field of the form carefully and attach the collected documentation. Pay any required fees (often a government application fee plus an ongoing renewal fee). You may also request a pre-application meeting with the regulator to clarify any points.

- Regulatory Review & Approval: After submission, regulators will thoroughly review your filings. They may ask for clarifications or additional evidence. Approval timelines vary significantly: some jurisdictions (like Lithuania or Estonia) may issue approvals in 1–3 months, whereas others (e.g. France or the U.S.) can take 6–9 months or more. Maintain open communication, respond promptly to inquiries, and be prepared for audits of your systems.

- Ongoing Compliance: Once registered, maintain compliance continuously. Keep AML/CFT programs updated, file periodic reports (e.g. transaction reports, auditor attestations), and renew your registration as required. Non-compliance after approval can lead to license revocation.

“In completing and submitting the required registration information, Applicant Firms must satisfy the Central Bank that they are fully compliant with all relevant regulatory requirements under the CJA 2010 to 2021.”

Throughout this process, align closely with the requirements of the jurisdiction. For instance, Ireland mandates a pre-registration notification and digital account setup, while U.S. FinCEN requires you to register as a Money Services Business within 180 days of starting crypto services. Consulting specialists (like 7BaaS’s licensing team) can help navigate country-specific rules.

Here’s a quick checklist of tasks when applying:

- Bullet List of Licensing Steps:

- Establish your company (incorporation, shareholding).

- Draft full AML/CFT policies and KYC procedures.

- Collect directors’ resumes, criminal background checks, and financial statements.

- Prepare a technology/security report (custody protocols, encryption methods).

- Complete and submit the regulator’s registration form with attachments.

- Pay application fees and prepare for any interviews.

- Implement any requested changes and await approval.

- Establish your company (incorporation, shareholding).

Key Compliance Requirements for VASPs

Obtaining registration is only the beginning. Regulators expect registered VASPs to maintain stringent compliance measures on an ongoing basis. Key obligations for a crypto wallet VASP include:

- AML/KYC Policies: Implement a risk-based AML program. Verify the identity of every customer (KYC) before allowing transactions. Use multi-factor ID checks for high-risk users. Maintain up-to-date KYC records in secure systems.

- Transaction Monitoring & Reporting: Continuously monitor wallet transactions for suspicious patterns (large transfers, rapid fund movements, etc.). Have procedures to report any suspicious transactions to authorities. The FATF explicitly requires VASPs to have systems for transaction monitoring and suspicious activity reports.

- Travel Rule Compliance: Comply with “Travel Rule” regulations that require sharing sender and receiver information for crypto transfers. Both the UK and major markets (U.S., EU) now enforce Travel Rule obligations for VASPs. Prepare to exchange information with other crypto firms to trace fund flows.

- Recordkeeping: Keep detailed records of all transactions, KYC documents, and internal risk assessments, typically for at least five years. Regulators will audit these records to confirm compliance.

- Cybersecurity and Data Protection: Secure your wallet infrastructure against hacks and data breaches. Employ strong encryption, offline key storage, and routine security audits. Protect customer data in compliance with privacy laws (e.g., GDPR in the EU).

- Governance and Audits: Appoint a dedicated compliance officer and establish a compliance committee. Periodically audit your own controls (internally or via third parties) to demonstrate to authorities that your AML/CFT measures are effective.

- Financial Requirements: Some jurisdictions impose minimum capital or insurance requirements on VASPs. For example, many require that operators hold a certain net worth or maintain professional indemnity insurance.

Meeting these requirements demonstrates responsibility and builds credibility. For instance, FATF guidance notes that licensed VASPs “have the same full set of obligations as financial institutions”. In practice, this means a crypto wallet service must treat AML/KYC as non-negotiable.

Best Practices: Automate KYC/AML checks using fintech compliance tools. Implement real-time transaction alerts. Stay informed on updates (e.g. EU’s MiCA regulations or national crypto laws) and update policies proactively. Document all procedures clearly – regulators evaluate the effectiveness of your policies during registration and subsequent inspections.

Common Challenges and Best Practices

Registering and running a compliant crypto wallet service can be complex. Some common challenges include:

- Evolving Regulations: Crypto laws are rapidly changing. For example, the EU’s Markets in Crypto-Assets (MiCA) framework is introducing new EU-wide rules, and global anti-money laundering standards are tightening each year. Stay updated on relevant developments (via FATF, local regulators, and industry updates) and adjust your compliance framework accordingly.

- High Compliance Costs: While company registration may be straightforward, building and maintaining AML compliance is resource-intensive. Costs include technology (AML/KYC software), hiring or consulting with compliance officers, and covering audit fees. Budget wisely and treat compliance spending as an investment in business sustainability.

- Long Approval Times: Some regulators have lengthy review processes. For example, France’s AMF or the US Bank Secrecy Act (via FinCEN and state money transmitter licenses) can involve 6+ month timelines. To mitigate delays, prepare documentation meticulously and respond promptly to any questions. Seeking pre-application advice from the regulator can also speed up approval.

- Cross-Border Operation: If you plan to serve users in multiple countries, you may need multiple registrations. For instance, offering services to U.S. customers typically requires FinCEN/MSB registration (and possibly state licenses), while serving EU customers may eventually trigger MiCA licensing. A careful jurisdiction strategy is needed—opt for one country as your base, then expand.

- Technological and Cyber Risks: Wallet services are targets for cyberattacks. A security incident can attract regulator scrutiny or license revocation. Invest in top-tier cybersecurity, regular penetration testing, and insurance.

Solutions and Tips: Engage experienced legal and compliance advisors (such as 7BaaS) early in the process. Leverage established compliance solutions for automated KYC/AML checks. Keep your business plan and risk assessments transparent with regulators. Involve compliance teams in product design (e.g. building regulatory requirements into your wallet software). Adopt clear internal policies and ensure all staff are trained on AML protocols.

By recognizing these challenges upfront and following best practices, documenting procedures, maintaining open communication with regulators, and continuously improving your compliance program—you can significantly streamline the VASP registration journey and maintain regulatory goodwill.

Conclusion

Launching a crypto wallet service legally requires more than just technology; it demands rigorous adherence to financial regulations. This VASP compliance guide has shown that you must treat your wallet business as a regulated financial entity. From registering as a VASP with the relevant authority, to implementing comprehensive AML/KYC programs, each step is vital. Remember that global bodies like the FATF mandate licensing or registration, and national regulators (e.g. the UK’s FCAf or Ireland’s Central Bank) will enforce these rules.

7BaaS has deep expertise in crypto licensing and regulatory compliance. By leveraging their consulting services, fintech startups and blockchain companies can navigate these complex requirements with confidence. Contact 7BaaS today to get tailored guidance on VASP registration, crypto AML compliance, and secure your wallet service’s legal standing. With the right support, you can focus on innovation knowing your compliance obligations are fully met.

FAQs

What is a VASP license or registration?

A VASP (Virtual Asset Service Provider) license/registration is official authorization to operate cryptocurrency services under the law. It means the company is recognized by regulators as a licensed crypto business and is subject to AML/CFT regulations. Essentially, a VASP license allows an exchange, wallet, or similar service to legally handle virtual assets.

Does my crypto wallet service need to register as a VASP?

If your wallet service holds or transfers crypto on behalf of users (making it a custodial or transactional service), then yes. Such activities typically fall within the definition of a VASP. Global regulators (FATF, FCA, etc.) require VASPs to register for AML oversight. Non-custodial wallets that do not touch private keys may have lighter obligations, but most professional wallet providers must register.

What steps are involved in registering a crypto wallet service?

First, form a corporate entity and gather all company documents. Next, build an AML compliance framework (KYC processes, risk management, etc.). Then, prepare and submit the detailed application dossier to the financial regulator, including business plans and AML policies. Finally, engage with the regulator during the review. (See steps above for a detailed process.)

How long does VASP registration typically take?

It varies by jurisdiction. Fast-track crypto-friendly countries like Estonia or Lithuania may approve within 1–3 months. Others (for example, the U.S. FinCEN/MSB registration plus state licenses, or European authorizations under MiCA) can take 6–9 months or longer. Plan accordingly and apply early, as timelines depend on the completeness of your application and regulatory workload.

What are the consequences of not registering my crypto wallet service?

Operating without required registration is illegal. You may face fines, business shutdown, or criminal charges. For instance, Ireland’s law explicitly makes unregistered VASP activity an offense. In practice, banks and partners will also refuse to work with an unlicensed crypto business. Registration ensures you can operate safely and maintain trust.