Buying or selling a licensed financial company – such as an EMI (Electronic Money Institution), MSB (Money Services Business), or crypto exchange – is a strategic M&A move that bypasses lengthy licensing processes. How to buy or sell a licensed financial company requires navigating regulatory approvals, compliance frameworks, and due diligence. This guide explains what it means to acquire or exit a licensed entity, common types of fintech licenses involved, the benefits of a pre-licensed acquisition, key legal considerations, and how 7BaaS can assist buyers and sellers.

What Does It Mean to Buy or Sell a Licensed Financial Company?

Buying a licensed financial company means acquiring the corporate entity that holds a regulatory license (e.g. for money transmission, payments, e-money, or crypto services). In practice, licenses themselves cannot simply be transferred by selling assets. Instead, buyers typically purchase the company’s shares so that the license remains with the same legal entity. For example, a fintech startup might buy a UK EMI-licensed firm to instantly gain an FCA-regulated payments license, rather than applying for a new license under PSD2. Selling a licensed business (exit) involves transferring ownership while ensuring the licensee’s compliance program remains intact. In both cases, regulators (FCA, central banks, FinCEN, FINTRAC, etc.) often require notification or approval of a change in control before or after closing.

In essence: the buyer gains a ready-made license, infrastructure, and client base, while the seller hands off an operating, regulated company. However, each step – from valuation to final handover – must account for regulatory filings and approvals. For fintech founders or investors, this path can offer a fast market entry or exit, but only with careful legal and compliance planning (e.g. structuring the deal as an equity acquisition since “licenses aren’t transferable”).

Common Types of Licensed Financial Entities Bought or Sold

Licensed financial companies come in various forms across different jurisdictions. Common targets for acquisition or sale include:

- Electronic Money Institutions (EMIs): Licensed under e-money/directives in the EU/UK to issue digital money and payment services.

- Payment Institutions (PSPs): Firms authorized under PSD2 (EU) or PSR (UK) for payments and money remittance.

- Money Services Businesses (MSBs): In the US, Canada, and other countries, MSBs (money transmitters, check cashers, currency exchangers) must register or license (e.g. FinCEN registration in the US, FINTRAC in Canada).

- Virtual Asset Service Providers (VASPs): Crypto exchanges and custodians requiring AML/crypto licenses in many jurisdictions (e.g. FINTRAC/VASP registration in Canada, FinCEN in the US, or FCA in UK).

- Specialty Lenders and Fintech Banks: Entities with money transmission, lending, or limited banking licenses (like Canadian Payments Service Act companies, or payment bank charters).

- Platform Shells and Startups: Pre-registered companies that have secured a license but have not launched products, often in jurisdictions like Malta, EU, UK, or offshore financial centers.

For instance, 7BaaS’s marketplace has listed Canadian MSBs and PSPs, a Portuguese bank account for an expat company, and an operational Maltese EMI as acquisitions. Sellers might offer a crypto license from the Czech Republic or a European DSP license company. Essentially, any regulated fintech or crypto company with an intact license and bank ties can be on the table.

Benefits of Buying a Pre-Licensed Company

Acquiring a licensed entity has several advantages over applying for a new license:

- Speed to Market: The company already holds regulatory approval, so you can begin operations (or scale existing ones) immediately after closing, rather than waiting months for a new license. For example, 7BaaS notes that some MSB transfers can complete in a week when all is prepared.

- Established Infrastructure: You inherit existing banking relationships, payment processor connections, core systems, and compliance frameworks. This saves time and reduces startup costs.

- Existing Revenue/Client Base: If the target is operational, it may have active clients, transaction history, and revenue streams, which can boost valuation and shorten ROI time.

- Regulatory Authority Approval: Because the entity is already regulated, less uncertainty exists about meeting licensing requirements.

- Lower Risk of Rejection: Building a new license application can be risky, especially in strict jurisdictions. Buying an approved company sidesteps the uncertainty of the initial licensing review.

However, buyers must also assume any inherited risks (legacy compliance issues, pending investigations, etc.). The benefit is a “license in hand” advantage: a ready-made fintech platform instead of a long, uncertain startup process.

Legal and Regulatory Considerations

Regulatory Change-of-Control: Most financial licenses have strict “change of control” rules. In the UK, the FCA requires notification and prior approval if you acquire control of a regulated payment or e-money firm. Similarly, EU directives often treat ownership changes as a new licence application (e.g. EMD2 or PSD2). In the U.S., state money transmitter licenses typically define “control” as 10–25% ownership, triggering new state filings. FinCEN (U.S. MSB registry) requires each MSB to keep registration details current – there is no official “transfer” procedure. In Canada, selling an MSB means the purchaser must update FINTRAC’s registry and risk assessment.

Licenses Are Not Transferrable: By law, you generally cannot sell a license as an asset. Instead, deals are structured as equity (share) transactions so the license remains with the same legal entity. This means the buyer inherits the licensed company entirely (assets, liabilities, contracts, and license). Often the purchase agreement includes conditions precedent for regulators to approve the change of control before closing. For instance, Goodwin LLP notes that U.S. state regulators may require detailed applications and impose wait periods (30-90 days) for money transmitter license approvals. Similarly, FCA change-in-control notifications have a 60 working-day review period.

Compliance and AML/CTF: Any acquisition must maintain anti-money laundering (AML) and know-your-customer (KYC) programs. Regulators expect continuity of robust compliance. Buyers should review the target’s customer risk profiles, suspicious activity reports, and internal audit history. Banks will also review the transaction (many licenses require bank approval too). If selling a crypto or high-risk business, ensure AML policies meet the latest FATF-style guidelines.

Jurisdictional Variances: Each regulator has unique rules. For example, FCA’s FSMA Section 178 regime covers PIs and EMIs, whereas FCA-registered crypto firms (exchange/custodian) fall under Money Laundering Regs with similar controls. The U.S. approach can involve dozens of state filings for MTL licenses. The EU often requires notifying the national central bank or central EMI register. 7BaaS clients operate globally, so they juggle UK/EU (FCA, EBA guidelines), North America (FinCEN, FINTRAC, state regs), and other markets (GCC, Asia). Key point: Always verify the controlling “fit and proper” of new owners with each regulator’s criteria before closing.

Data and Contracts: A sale may transfer customer data between different owners. Data protection laws (GDPR, PIPEDA, etc.) must be considered, and customers may need to consent to the new ownership. Contracts with partners (card networks, tech providers) often require assignment or novation clauses. Bank account signatories usually must be updated, and may trigger de-banking if not handled correctly. 7BaaS ensures legal counsel addresses these issues.

Financial and Tax: Ensure clarity on selling price allocation (assets vs goodwill) for tax. Some jurisdictions charge fees for license applications or transfers (e.g., FCA has fees for change-in-control applications). Ongoing capital requirements or trust reserve transfers may be part of negotiations (especially for MSBs with trust accounts).

Due Diligence Checklist for Buyers

A thorough due diligence is critical. Key items include:

- License & Registration Records: Obtain a complete list of all regulatory licenses, registrations, exemptions and filings (including IDs and renewal dates). Document any pending applications. This verifies scope (e.g. does a US MSB also have licensure for currency exchange and check cashing, or only money remittance).

- Regulatory Correspondence: Review all communications with regulators – audit reports, notices of non-compliance, enforcement actions, or pending change-of-control filings. Identify any “red flags.”

- Compliance Program: Examine AML/KYC policies, training records, SAR/STR filings, and compliance officer credentials. Look for any lapses or outstanding issues. Ensure risk assessments and suspicious transaction reporting procedures exist.

- Financial Statements & Bank Records: Audit financials for accuracy. Check bank statements for any unusual transactions. For MSBs, verify trust account funding and usage. Ensure there are no hidden liabilities or lawsuits.

- Customer Base and Contracts: Analyze customer mix (retail vs corporate, industries served, geographies). Check major contracts (payment processors, partners, merchant agreements) for change-of-ownership clauses.

- Management and Shareholders: Background-check all directors, officers, and 10%+ shareholders. In many jurisdictions, regulators will review new officers’ fitness and may require clearance for them.

- Technology and IP: Confirm ownership of any key software or platform. Check cybersecurity measures. See if intellectual property (trademarks, patents) are properly assigned to the company.

- Insurance and Bonds: Verify any fidelity bonds, AML insurance, or guaranties required by law. Ensure policies will continue or transfer to new owners.

- Tax and Legal: Review tax compliance, filings, and any disputes. Ensure corporate governance documents (articles, shareholder agreements) are in order.

For example, Goodwin LLP suggests demanding a change-of-control chart: a table showing for each license what filings or approvals are needed for the new owner. This should include timelines and regulator contacts. In due diligence, 7BaaS also prepares a regulatory dossier summarizing licensing requirements and any quirks (e.g. certain U.S. states might define “control” at 5% ownership). A diligent checklist prevents last-minute surprises and helps structure the deal properly.

Figure: Team-based due diligence and planning are crucial when acquiring a regulated fintech company.

How to Structure a Purchase or Sale

Once due diligence is done, structure the transaction with these best practices:

- Equity vs Asset Deal: As noted, licensed-company deals are almost always structured as equity (share or membership interest) purchases, not asset sales. This allows the license to stay with the entity. If an asset sale were done, the buyer would need to apply for a new license.

- Deal Timeline and Milestones: Incorporate a “sign & close” approach. The purchase agreement is signed under the condition that regulators approve the change of control before or at closing. If approvals drag on, the deal can include a fixed waiting period or staggered closing. 7BaaS often suggests escrow arrangements: a portion of purchase funds is held until final transfer of control.

- Condition Precedents: Key conditions usually include obtaining all necessary regulatory consents (bank and license approvals), no material adverse change in the business, and financing clearance. The agreement should obligate the seller to cooperate on filings.

- Purchase Price Adjustment: Factor in any compliance deficiencies. For example, if due diligence reveals missing capital or incomplete AML controls, the buyer may hold back funds or require the seller to cure issues.

- Transition and Support: Negotiate post-closing transition assistance – e.g. the seller’s key compliance staff might stay on for a period to train the buyer’s team. This ensures continuity of anti-fraud measures and risk policies. 7BaaS itself can act as a consultant during handover.

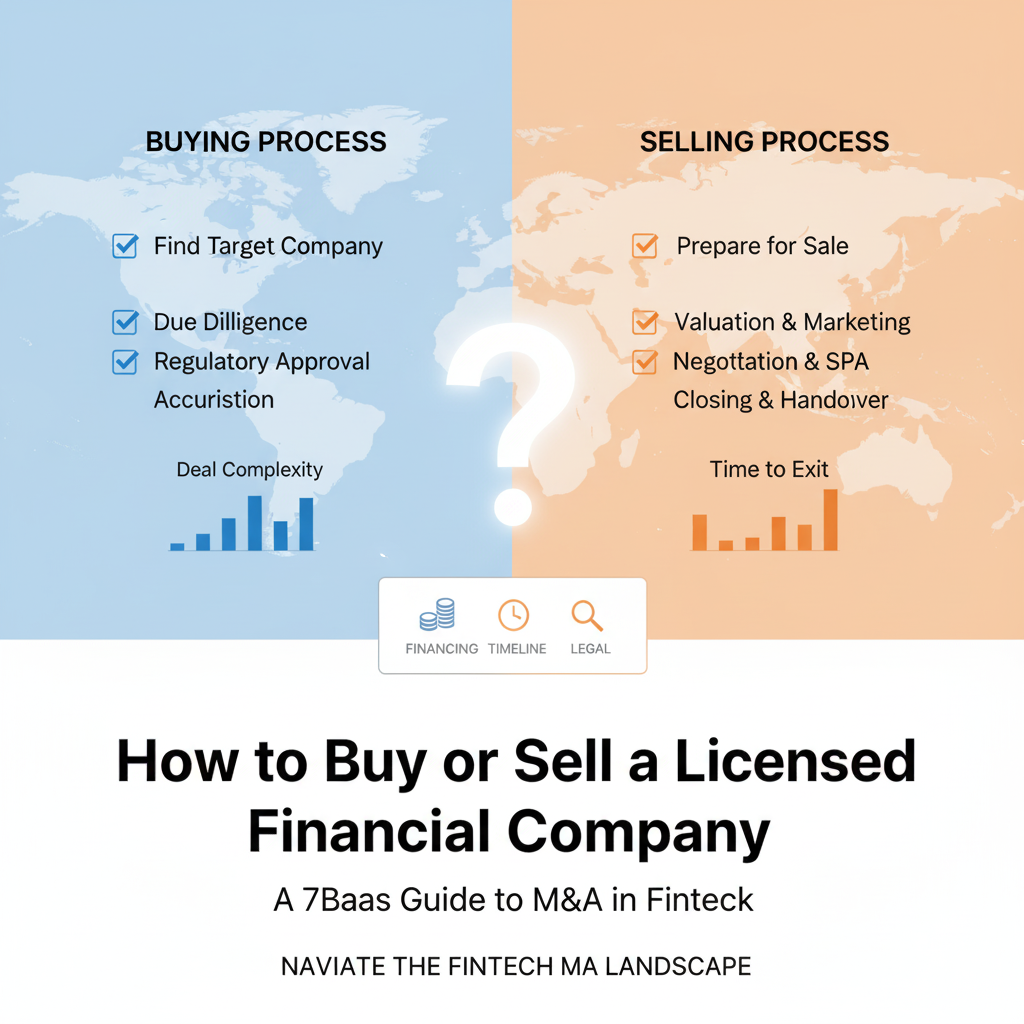

- Step-by-Step Process: In 7BaaS’s experience, licensed company deals follow a clear sequence: 1) Discovery & NDA – sign non-disclosure and outline objectives. 2) Valuation & Planning – agree on price and structure. 3) Dossier/Data Room – compile all documents for buyer’s diligence. 4) Offers & Negotiations – finalize terms. 5) Regulatory & Banking Filings – submit change-of-control notices to regulators and banks. 6) Closing & Handover – complete sale once approvals arrive, transfer shares, update filings.

By following a structured approach and working with advisors, parties can avoid common pitfalls. For example, regulators often impose strict deadlines (the FCA uses a 60-working-day clock once a complete notification is filed), so parties must prepare filings well in advance of projected closing.

Timelines and Costs Involved

Each transaction is unique, but some general expectations are:

- Deal Timeline: Typically, buying or selling a licensed company takes several weeks to a few months. 7BaaS cites an average deal window of 6–10 weeks from NDA to closing, though complex cases may stretch longer. Regulatory approval is often the rate-limiting step – for example, FCA clearance up to 60 days, U.S. state licenses ~1–3 months, and bank account changes ~2–6 weeks. In many cases, the bulk of the work (diligence, documentation) happens quickly, but closing waits on official approvals. Some simple MSB acquisitions (with no major issues) have been done in about a week once everything was ready, but plan for a couple of months to be safe.

- Costs: Beyond the purchase price, buyers should budget for professional fees: legal counsel, accountants, and specialized compliance advisors. Regulatory filing fees can be significant (for example, the FCA charges a fee for each change-of-control notification). If the deal involves multiple jurisdictions, each regulator may charge. Additional costs include corporate restructuring (e.g. new legal filings), updates to AML software or bonding requirements, and possibly new compliance hires. 7BaaS offers transparent pricing for its advisory services, so clients know advisory fees upfront.

- Unexpected Delays: High-risk licenses (like crypto) or distressed sellers might slow approvals (some regulators demand extended background checks or remedies for non-compliance). Hence, it’s wise to include buffer time and clear termination rights if delays exceed agreed timelines.

Despite these costs, buying a licensed company often saves years of expense versus a fresh license application. The key is anticipating regulatory steps and budgeting accordingly.

How 7BaaS Supports Buyers and Sellers

7BaaS specializes in facilitating licensed company transactions worldwide. Our role includes:

- Marketplace & Deal Flow: Through the 7BaaS platform, buyers gain access to verified listings of EMIs, MSBs, VASPs and other licensed entities. Sellers can confidentially list their companies. 7BaaS vets each opportunity, ensuring licenses are active and dossiers are complete.

- Valuation & Advisory: 7BaaS experts help value licensed entities fairly (often using revenue multiples or compliance cost savings). We advise on negotiation strategy to maximize the seller’s return while keeping buyers within budget.

- Due Diligence Assistance: We organize data rooms and checklists aligned with regulatory expectations. Our team highlights any red flags and suggests mitigation (e.g. strengthening AML before sale). For buyers, we consolidate compliance documentation so regulators have what they need.

- Regulatory Filings: 7BaaS prepares or reviews all change-of-control filings and liaises with regulators/banks. We know, for instance, which states require fingerprint cards or background forms for an MSB, or which directors must be replaced under an EMI’s terms. This expert handling accelerates approvals.

- Compliance Framework: Post-transaction, we can integrate the acquired compliance policies into the buyer’s operations. For sellers, we ensure all reporting (e.g. to FinCEN or FINTRAC) is updated and closed out properly.

“Why buy, sell & refer with 7BaaS: Trust and compliance come first. Whether you’re buying, selling, or referring to licensed companies, our experts ensure that every transaction is handled securely, strategically, and in full alignment with legal and regulatory standards. 7BaaS offers Licensed Company Sales expertise (structuring deals for compliance) and Strategic Buying Support (access to vetted targets and end-to-end due diligence).”

By combining fintech M&A know-how with regulatory depth, 7BaaS turns a complex acquisition into a smooth process. We act as a single point of contact: from initial discovery (NDA stage) through to closing and post-sale integration. This integrated service is unique in the marketplace and ensures clients – whether buyers or sellers – don’t run into unforeseen compliance roadblocks.

Conclusion & Call to Action

Navigating how to buy or sell a licensed financial company requires a blend of business strategy and regulatory savvy. The benefits of acquiring an existing license can be huge – rapid market entry, proven infrastructure, and instant credibility – but only if done correctly. Key steps include assembling a strong due diligence team, structuring the deal as an equity acquisition, satisfying all change-of-control requirements, and budgeting for approval timelines.

7BaaS is your global partner in this process. We specialize in connecting buyers and sellers of licensed fintech firms and guiding them through every regulatory and logistical hurdle. Ready to buy or sell a licensed financial company? Contact 7BaaS today for a free consultation. Our experts will explain how our Marketplace and consulting services can maximize the value and speed of your acquisition or exit, ensuring full compliance every step of the way.

Explore licensed fintech deals on 7BaaS, or schedule a consultation to learn how we can make your licensed company acquisition or sale seamless and fully compliant.

FAQ

Q: What are the main steps when buying a licensed financial company?

A: Key steps include signing an NDA and preparing valuation, compiling a detailed data room for due diligence, submitting regulatory change-of-control filings, and closing once approvals are granted. You’ll need to review the target’s licenses, compliance program, finances, and contracts, then structure the deal as an equity purchase since licenses aren’t transferable by asset sale.

Q: Can I transfer a financial license to a new owner?

A: Not directly. Most regulators (FCA, FinCEN, etc.) do not allow a license to be “sold” as an asset. Instead, the licensed company’s ownership shares are transferred. The regulator then reviews the change of control. For example, Goodwin LLP notes that “Licenses can’t be transferred…licensee acquisitions have to be structured as securities/interests deals”. After the sale, you must update the licensee’s regulatory registration (or bank forms) to reflect the new owner.

Q: How long does the acquisition of a licensed company usually take?

A: It varies, but expect 6–12 weeks or more in many cases. Due diligence and negotiation might be done in a few weeks, but regulatory approvals can take additional time (the FCA allows up to 60 working days after a complete notification). 7BaaS typically sees deals closing in about 6–10 weeks on average, but complex cases or multiple licenses can extend this. We help clients set realistic timelines and follow up with regulators to avoid delays.

Q: What kinds of licensed financial companies does 7BaaS help with?

A: 7BaaS focuses on regulated fintechs globally. This includes Electronic Money Institutions (EMIs) and Payment Service Providers in Europe/UK, Money Services Businesses (MSBs) in North America, Virtual Asset Service Providers (VASPs/crypto exchanges), and other licensed entities. As noted on our platform, we’ve handled sales of Canadian MSBs, European EMIs, and crypto licenses, among others.

Q: How does 7BaaS support compliance during a transaction?

A: Regulatory compliance is integral to our service. We manage all legal and compliance obligations on your behalf. This includes updating AML/KYC policies, ensuring accurate regulatory filings, and coordinating with legal counsel. For example, our Compliance Consulting and Company Formation teams can provide ongoing AML program development and ensure the new ownership meets all “fit and proper” requirements. We aim to handle each deal in a way that is “secure, strategic, and in full alignment with legal and regulatory standards”