Introduction

Canada’s fintech ecosystem is thriving. As digital payments, cross-border transfers, and online marketplaces continue to expand, the demand for robust Payment Service Providers (PSPs) has never been higher. PSPs play a central role in the financial infrastructure — enabling merchants and fintechs to process payments, manage settlements, and comply with anti-money laundering (AML) and Know Your Customer (KYC) regulations.

However, for entrepreneurs and investors looking to enter this space, one key decision often arises early on: Is it better to build a PSP from scratch or to acquire an existing one?

While starting a PSP allows full customization and control, it also demands time, complex regulatory approvals, and heavy upfront investment. In contrast, acquiring an existing PSP — one that is already licensed, compliant, and operational — can dramatically accelerate market entry and reduce risk.

This article explores why buying an established PSP in Canada can be a faster, more strategic route compared to launching a new one. From regulatory frameworks and due diligence to integration timelines and market credibility, we’ll unpack every factor that matters to fintech founders, private equity firms, and institutional investors eyeing the Canadian market.

1. Understanding the Canadian PSP Landscape

The Canadian payments industry operates under a well-defined regulatory structure. PSPs are overseen primarily by the Bank of Canada under the Retail Payment Activities Act (RPAA) and by FINTRAC under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA).

Any company that facilitates the transfer of funds between parties — whether through card processing, e-wallets, cross-border remittances, or digital platforms — falls under the PSP definition.

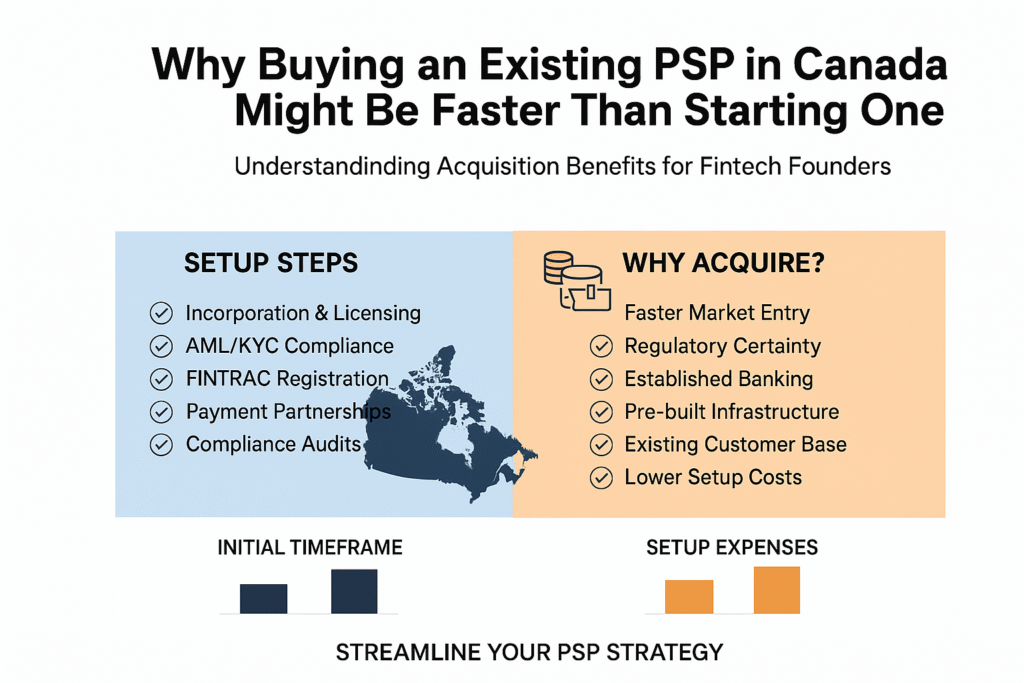

Setting up a new PSP involves:

- Incorporating a legal entity in Canada.

- Drafting AML and KYC compliance programs.

- Completing the FINTRAC MSB registration (if applicable).

- Registering under the RPAA.

- Establishing banking partnerships and payment rails (e.g., SWIFT, SEPA, Visa/Mastercard connections).

- Undergoing multiple compliance audits before going live.

Each of these steps can take months, sometimes over a year, before a PSP becomes fully operational. By contrast, acquiring an existing PSP allows new owners to leverage an already established structure, reducing time-to-market significantly.

2. Regulatory Readiness: The Key Accelerator

In Canada, obtaining a PSP registration or a Money Services Business (MSB) licence is not just a formality; it involves detailed regulatory vetting. FINTRAC requires documentation on ownership, management, compliance policies, and criminal background checks. The Bank of Canada also reviews governance frameworks and operational resilience.

Building this from the ground up takes time — sometimes up to 12–18 months.

When you buy an existing PSP, you inherit a company that’s already passed these stages. The PSP’s existing FINTRAC registration and RPAA compliance framework can remain intact, subject to ownership updates. This means:

- No waiting for new regulatory approvals.

- No initial FINTRAC or Bank of Canada delays.

- Immediate operational capacity under existing licences.

However, it’s essential to perform thorough due diligence to ensure that the PSP’s compliance record is clean. Acquiring a PSP with a strong compliance history not only saves time but also builds credibility with financial institutions and regulators.

3. Speed to Market: A Strategic Advantage

For fintech entrepreneurs, time is a competitive advantage. Launching a new PSP means months of documentation, regulatory engagement, and banking negotiations before accepting the first transaction.

Acquiring an existing PSP can cut this process by more than half. You gain:

- Existing customer base and transaction history, which builds trust with banks and investors.

- Pre-configured payment infrastructure, including gateways, merchant accounts, and APIs.

- Established banking and card network relationships, which are often the hardest to secure as a new entrant.

This allows investors or founders to begin operating almost immediately after acquisition, focusing on expansion and innovation rather than compliance setup.

For example, instead of waiting 12–18 months for licensing, the buyer can enter the market in as little as 2–3 months by completing due diligence, ownership transfer, and integration.

4. Cost Efficiency and Reduced Setup Expenses

Starting a PSP from scratch requires significant financial investment before any revenue is generated. Initial expenses often include:

- Legal and consulting fees for regulatory registration.

- AML/KYC compliance framework development.

- Banking relationships and payment network integration.

- Technology infrastructure and risk management systems.

These costs can easily reach hundreds of thousands of dollars, with no guaranteed approval timeline.

By contrast, when you buy a PSP, much of this infrastructure is already in place. The initial purchase price may be substantial, but it consolidates licensing, operational setup, and early-stage costs into one transaction.

Moreover, existing PSPs typically come with pre-negotiated processing rates and established transaction flows, reducing both operational and opportunity costs.

5. Banking and Partnership Access

One of the greatest challenges for a new PSP in Canada is building banking relationships. Canadian financial institutions are cautious when onboarding fintechs or MSBs due to AML/ATF risk considerations.

Acquiring an existing PSP allows you to inherit banking and network relationships that may have taken years to develop. This provides immediate access to:

- Settlement accounts.

- Payment rails and clearing partners.

- Merchant onboarding systems.

- Risk and fraud monitoring tools.

Maintaining these partnerships is crucial. Banks prefer dealing with entities that have a proven compliance history and clean operational record. Buying a PSP that already enjoys such relationships drastically shortens the timeline to start transacting.

6. Established Compliance and AML Framework

Compliance is at the core of any PSP operation in Canada. Regulators expect PSPs to maintain robust anti-money laundering programs, customer verification procedures, suspicious transaction monitoring, and independent audits.

Developing this framework from scratch involves:

- Writing compliance manuals and risk assessments.

- Conducting staff training programs.

- Implementing reporting mechanisms to FINTRAC.

- Setting up independent audit systems.

This takes months and requires expertise in regulatory interpretation.

When you buy an existing PSP, you acquire a tested compliance framework. While you should still review and strengthen it to reflect your business model, the foundation already exists — saving months of effort and reducing the risk of regulatory missteps.

7. Brand Recognition and Market Credibility

Market trust is critical in financial services. A PSP that has already been operating in the Canadian market enjoys brand recognition and a transaction history that signals reliability.

Launching a new PSP means starting from zero — building relationships, gaining client trust, and demonstrating compliance credibility. Conversely, acquiring an existing PSP allows you to leverage its operational history, audited records, and client references.

For investors or international fintechs entering Canada, this reputation can be invaluable. It facilitates faster onboarding of new clients, easier access to capital, and smoother negotiations with banks and regulators.

8. Shorter Integration Timelines and Immediate Scalability

Modern PSPs operate through complex integrations — payment gateways, API systems, and merchant dashboards. Building these from scratch requires both technical development and security certification.

By acquiring an existing PSP, you gain ready-made infrastructure that can be integrated into your operations quickly. This means:

- Shorter software deployment timelines.

- Immediate merchant transaction processing capability.

- Ability to scale operations regionally or globally with fewer interruptions.

In short, acquisition doesn’t just save regulatory time — it also fast-tracks technology readiness and scalability.

9. Risk Considerations When Acquiring a PSP

While buying an existing PSP offers speed and efficiency, it comes with its own risks that must be managed through due diligence. Key areas to assess include:

- Regulatory compliance record: Ensure there are no unresolved FINTRAC or Bank of Canada warnings.

- Financial statements: Review audited accounts to confirm profitability and sustainability.

- Client and partner contracts: Identify any legal restrictions on ownership transfer.

- AML/KYC procedures: Verify that all required controls are current and effectively implemented.

- Technology and cybersecurity: Ensure systems meet data protection standards.

Conducting a full compliance audit before acquisition helps prevent inheriting hidden liabilities. It’s also wise to engage Canadian legal and compliance advisors to navigate the ownership transfer process smoothly.

10. Operational Flexibility and Strategic Growth

Once the acquisition is complete, the buyer gains immediate operational flexibility. Unlike starting a new PSP, which requires initial months of setup, the acquired PSP can be repositioned strategically.

For example, you may:

- Expand into new segments such as e-commerce payments, remittances, or card issuing.

- Rebrand the PSP to align with your corporate identity.

- Introduce new digital services using the same regulatory framework.

Because the licensing and compliance structures are already established, you can focus on innovation, growth, and revenue generation instead of setup compliance.

This strategic agility is a core reason many investors prefer buying a PSP over building one from the ground up.

11. Comparing the Timelines: Acquisition vs. Startup

| Stage | Starting a New PSP | Buying an Existing PSP |

| Incorporation & licensing | 6–12 months | 1–2 months |

| Banking relationships | 3–6 months | Already established |

| Compliance framework | 4–6 months | Already in place |

| Technology & systems setup | 3–5 months | Existing platform |

| Market entry | 12–18 months | 2–3 months |

| Total estimated timeline | Up to 18 months | Under 3 months |

This comparison clearly shows how acquisition drastically reduces the time to market — a decisive factor in a competitive fintech environment.

12. Long-Term ROI and Value Creation

Although purchasing an existing PSP involves an upfront cost, the return on investment (ROI) can be significantly higher in the long term. The immediate ability to operate, existing client base, and reduced regulatory friction make the investment worthwhile.

Moreover, owning a licensed PSP increases corporate valuation. Investors and partners view it as a regulated asset — a valuable gateway into the Canadian and global payment ecosystem.

With the ongoing rise of cross-border payment solutions, embedded finance, and virtual assets, acquiring a PSP now can position investors for exponential growth in the years ahead.

Conclusion

Acquiring an existing PSP in Canada provides a faster, more reliable, and strategically sound pathway into the regulated fintech market. It eliminates the lengthy setup process, reduces compliance uncertainty, and allows immediate access to existing systems, clients, and partnerships.

While due diligence and regulatory review remain essential, the benefits — speed, credibility, and scalability — far outweigh the challenges.

For entrepreneurs, fintech founders, and investors, buying a PSP isn’t just a shortcut; it’s a strategic investment decision that can define market success. With the right acquisition strategy and compliance preparation, your business can transition from planning to operating within months — ready to serve Canada’s fast-evolving payments industry.

References

- 7baas.com (Industry Insights on Fintech Licensing and PSP Advisory)

- 7baas.com/insights (Guides on MSB, PSP, and Compliance Strategies in Canada)